Five things on which I've changed my mind

From the Iraq War to raising income tax thresholds

In many ways I felt that I should write about the main political drama of the week - but couldn’t think of anything others hadn’t already said better. For those not totally satiated with Mandelson/Starmer drama, I can recommend these pieces by Fraser Nelson, Stephen Bush and Lewis Goodall.

My political views haven’t changed dramatically over the years. While I was much less politically engaged as a student, I would still have put myself on the right. But occasionally it’s worth looking back at some of the big things I’ve changed my mind on in politics - and what prompted me to do so.

Now, too many ‘changed my mind’ lists end up being, ‘once I believed in social democracy, but after much reflection I’ve realised I’m actually a democratic socialist’ or, ‘I used to support clause 32(a)(iii) of the Tax and Accountancy Act 1994, but now I don’t.’ And I could give you dozens of small shifts of that nature.

So the five items below are all ones where (a) they’re genuinely big issues; and (b) I’ve properly changed my mind; a 180 degree turn1 taking me from one side of the argument to another.

They are, in no particular order:2

The Iraq War

Raising income tax thresholds

French/Welsh style cultural protection

Lifting student number caps

Public Sector Pensions

The Iraq War

A classic one first: like around half of the population, I supported the war at the time, whereas now I think it was a mistake.3

Why did I support it? I believed the Government that Saddam Hussein either had, or was close to, obtaining weapons of mass destruction4 - and Saddam was clearly a bad guy, meaning I thought Iraq would be better off with him gone. The interventions in Kosovo and (as it seemed at the time) Afghanistan made foreign interventions look easy. I underestimated the challenges of nation building. And I didn’t (and still don’t) think that the consent of Russia and China makes a difference to whether or not a war is moral.

On an emotional level, I was probably irritated by the casual anti-Americanism and general lefty-ness of many of my fellow students,5 meaning a level of contrariness may have shaped my position.

My views have changed for much the same reason as everyone else’s. There were no WMDs, nation-building was hard, the cost was huge and the number of allied and Iraqi deaths, over the years, was immense. It squandered the good will of 9/11 and fractured the Western coalition that had gone into Afghanistan - and undoubtedly created the power vacuum which first enabled ISIS to flourish and strengthened Iran, both of which have caused as many problems down the line as Saddam did.6

Raising income tax thresholds

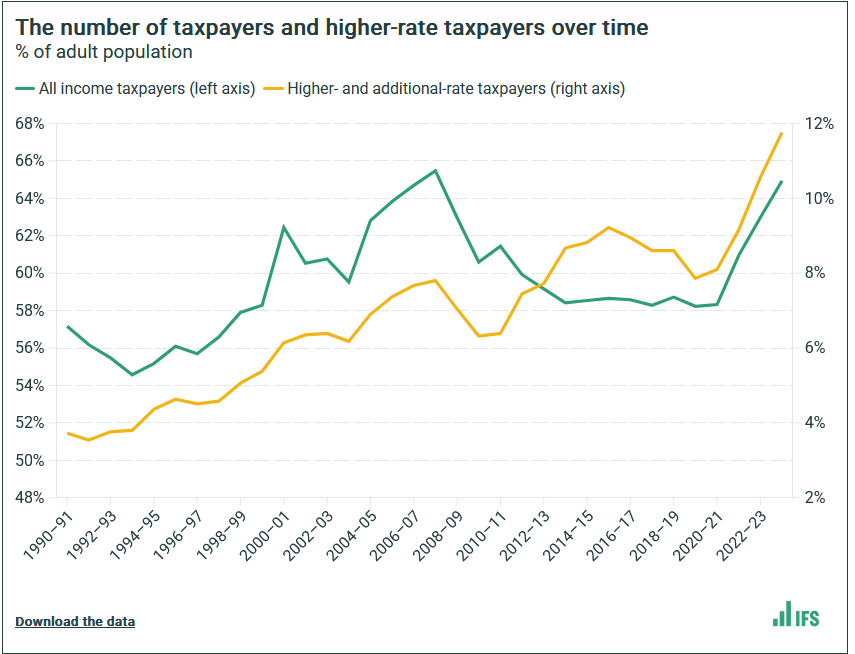

When the Coalition Government set out to raise the income tax threshold from c. £6,500 to £10,000 I was a big supporter. Although it was originally a Lib Dem policy, it was one I thought fitted fully with Conservative values.

It helped to make work pay - serving justice and strengthening the incentive to come off benefits. It was a tax cut, focused on the working poor who needed it most - and yet was universal, in that everyone benefited. I also felt the idea that we should tax low paid people, only to give a bunch of that money back via benefits, seemed pointless and inefficient: why should the government take with one hand and give back with the other?

Yet with hindsight, this was a mistake: a clear move away from the Lawsonian principle that taxation should be broad-based with low rates; i.e. that most people should contribute to some extent.7 Even if some of the money is ultimately given back, it would be better to have more people feeling they are contributing through tax, in order to maintain a stronger constituency for lower taxes.8

Following the reforms, more than 40% of adults were not paying any income tax at all. This is now down to just over a third - a much healthier state of affairs, and it is no coincidence that the pendulum on tax cuts vs tax rises has swung back as more people are dragged into the tax system. As someone who believes high taxes are economically damaging9, a broader base so that more people can directly feel the impact of higher public spending would be both beneficial and fairer.

To that extent, the recent freezes to the income tax threshold are a good thing. Of course, I’d have preferred them to be accompanied by a cut in the base rate of income tax (or, better yet, National Insurance10) alongside corresponding cuts to public spending. But raising the thresholds above inflation was a mistake - and restoring high-thresholds should not be a priority of a future tax-cutting government.

French/Welsh style cultural protection

I used to scoff at the way the French had language quotas for cultural preservation on the radio, or the Welsh government’s policy of relentlessly promoting Welshness via language, culture and history. Haha, how weak the French must think their culture is, to need such protections, I thought. Us in Britain have no need of such foolish things, as our culture is so great.11

But the reality is that any nation that wishes to survive as a nation needs to shore up its identity - which means an active, deliberate and ongoing programme of nation-building and cultural support. It is one of the most basic tests of whether you are a serious nation12 - and we can see that every nation (or similar) that is serious about its identity does this, whether it is small (Wales, Scotland) or large and powerful (the EU13, the US, China). Some in Britain mutter about North Korea every time this is suggested, but the truth is we have multiple democratic examples right on our doorstep.14

Even in Britain we used to do this - look at the Victorians! The idea we ‘don't do flags’ is a modern myth, dating to around the 60s and 70s, and perhaps one that was convenient for both those who regretted the loss of Empire, and those who were ashamed of its existence, to rally round.

In today's Britain - or rather England - we've moved from complacency to sabotage, with most of the institutions that should be at the forefront of maintaining our sense of self as a nation more interested in undermining it. Schools are more focused on highlighting areas of national shame rather than pride, while universities and museums openly adopt the anti-British, anti-Western ideology of ‘decolonisation’ to reorder their curricula and collections. Rather than the series it used to, such as Simon Schama's ‘A History of Britain’, the BBC chooses to commission David Olusoga's relentlessly anti-British ‘Empire’.15

This is not something that has public support. When polled, people - across every ethnic group - repeatedly show strong net agreement with statements such as ‘Britain, throughout its history, has been a force for good in the world’ or that ‘young people who grow up in Britain should be taught to be proud of Britain and its history.’ The approach taken by our schools, universities and museums has been a top-down cultural revolution, imposed by a small minority of the educated elites.16

And yet we can see the results of this relentless campaign of negativity in the attitude of young people, with only 41% of 18-27 year olds expressing pride in their country today, compared to 80% twenty years ago.17

Unlike the French and Welsh, our national language doesn't need protecting. But every publicly funded school and university, every publicly funded museum, and the BBC, should have an underlying duty to promote pride in Britain's history, heritage and culture.18 This doesn’t mean fabricating events, or banning the teaching of slavery. But it means an overall lens that is steadfastly dedicated towards pride, not shame. Again we don't have to look far to find an example of where this is done well. Visit Edinburgh Castle. They don't conceal that the English took Edinburgh at one point. But pride in Scotland oozes from every stone, along with a clear sense of satisfaction for every time they sent the English packing. And that - in Edinburgh - is exactly how it should be.

The biggest threat to Britain's continued survival, qua Britain, is not Russia, or China, or the EU, or Trump, or any external threat. It is simply that the British people give up any sense that Britain is something that is worth preserving, as an independent and united nation.

Lifting student number caps

You’ve seen me write about university over-expansion before, such as here, here and here. But believe it or not, when Willetts first said he was going to lift the caps on how many students each university could recruit, I thought it was a good idea.

Essentially I bought the argument that, ‘If Manchester wants to recruit more students, and more students want to go to Manchester, why should the state stop them?’ I believed that choice could be a powerful driver of quality - as it has been in schools, and in the private sector. And although I thought too many people were going, the numbers had been steadily increasing even with the caps, so I didn’t see this as a huge deal breaker.

In reality, what seemed like nice logic at the top of the sector had disastrous consequences. At the bottom end, thanks to no effective quality and standards oversight,19 we saw a huge proliferation of low quality courses, including in business studies and franchised providers, amongst other things. Higher tariff universities expanded rapidly, lowering their entry standards and degree standards to do so - all the while inflating grades, reducing staff/student ratios and over-crowding accommodation and lecture theatres. This in turn put yet more pressure on mid- and low- tariff providers, who faced further pressure to drop standards to recruit students, or else lay off staff.

Student choice also proved a poor driver of quality. In schools, strong external oversight and externally set exams provide robust information that parents can use to judge which schools are best. At university level, institutional autonomy meant it was all too easy for institutions to inflate grades or to dumb down content to inflate their National Student Survey results to climb the league tables. Removing the caps - alongside moving to an almost entirely fee-funded model - meant Government lost almost all influence on issues such as which courses should grow, regional provision or maintaining financial stability.

For some, that would have been a feature, not a bug. But we didn’t see the competition on price or quality that was promised. Instead, rather than competing on quality - as they used to - many universities chose to compete on size instead, with low interest rates fuelling an unsustainable splurge into facilities and infrastructure to attract new students, leaving debts that have come back to bite as interest rates rose.

Although student numbers rose when the caps had been in place, I also underestimated how much harder removing the caps would make it for government to put the genie back in the bottle. Rather than simply dialing the existing control mechanism into reverse, a whole new control mechanism would need to be added - a much harder political ask.

However, regardless of the issue of how many people should go to university, removing the caps was a disaster - as, increasingly, people who disagree with me about the ‘how many?’ question are also saying. The ‘market’ does not function in HE, it is a quasi market, backed by taxpayer funding, that has unleashed all the worst elements of competition - instability, reduction in standards and investment in wasteful conspicuous signalling - with none of the benefits, such as improved quality or lower costs. Regardless of whether you think more or fewer people should be going to university, institutional level caps need to be restored.

Public Sector Pensions

When I was in the civil service it seemed both right and proper that I should have an excellent defined benefit pension. After all, this was an appropriate reward for our lower salaries - and likely outweighed by the large bonuses and stock options enjoyed by our counterparts in the private sector. I felt this strongly: the one time I went on strike was due to pension changes.20

The arguments that final salary schemes were unaffordable I discounted, or rather felt it was artificially created, blaming it on Brown’s tax raid on pension fund dividends. The other thing that struck me as unfair about the defined contribution model was the degree of luck that surrounded a person’s final pension. Particularly when the requirement to buy an annuity was in place, two people retiring just a year apart with the same pension pot might have annual pensions 20% different in size.21 Surely pooling this sort of risk was exactly what Government should do - in fact, could it not encourage this sort of risk-sharing in the private sector, perhaps backed by large insurance firms?

I might have accepted my initial pension - a ridiculously generous final salary scheme accruing at 1/60 per year and takeable in full from 6022 - was a little lavish, but remained strongly in favour of a defined benefit scheme.

A lot of these things are partly true. Brown’s tax raid did have an impact, there was an unfairness regarding the timing of annuities23, and many private sector workers do get benefits - whether shares, bonuses, private health care or staff discounts - outside of their headline salary that the ‘what about the pension?’ crowd ignore.

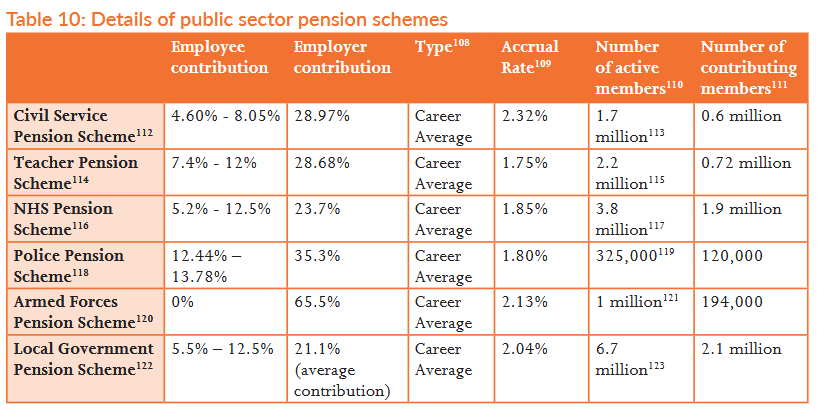

But it’s pretty clear that overall I was being biased by my own employment.24 Public sector pensions are, and remain, unreasonably high. Including bonuses, public sector pay is only 5% lower than the private sector - which cannot justify the disparity of 27% public vs 6% private average employer contribution into the pension.

Plus, of course, the public sector is more advantageous to employees in other ways, including greater job security, better terms and conditions (such as sick pay or maternity pay) and - at least for office based jobs - more working from home.25

Even if one did think the public sector (or parts of the public sector) should be paid more - perhaps to recruit and retain better staff - then having such a high proportion of total reward devoted to pension contributions would not be the way to do it.26 Employees notoriously undervalue their pension, and for retention and recruitment purposes it would actually be better to give a less generous pension and put more of that funding into increasing headline salaries. This is true whether we’re discussing getting more physics teachers to work in London, or compensating the very highest echelons (the only area where pay really does significantly lag the private sector equivalents) better.

A defined contribution funded pension scheme, with a standardised employer contribution of 10% and an employee contribution of 5%, would be much fairer. This aligns more closely with the best private sector schemes rather than the average, compensates for the 5% lower salary, and the total proportion of salary being invested into an employee’s pension, at 15%, is above the 12% recommended by Pensions UK for a suitable retirement.27 It would still be a good pension - just not an excessive one.

Lessons learned

So is there a common theme?

There isn’t an obvious directionality: in some I’ve shifted to the right, in others to the left.28 And they are on both economic and cultural matters.

There’s definitely a case that in some cases I was biased - either because the system personally benefitted me (public sector pensions) or played into my prejudices (the English being better than the French) - or to be more credible of ideas if they were coming from people I agreed with on other things.

There’s perhaps another commonality on putting too much confidence in theoretical models of how something should work - the power of choice, nation building - and not enough into how things could go wrong, or how the incentives might play out differently in the real world to in theory. These often look obvious in hindsight, but are hard to spot in advance.

Overall, beware of bias, beware of sympathy/antipathy, and pay more attention to second-order effects as well as theory aren’t bad lessons to take away - even if they can be easier said than done!

Or thereabouts. Maybe 150 or 160 degrees in some cases.

Not saying these are the only six. But I want to keep this piece to a manageable size!

Polls vary, and varied significantly on the conditions, but YouGov seems to think it was about half.

I can remember thinking the claims might have been somewhat ‘sexed up’, as the saying goes - but not that there’d be nothing behind them at all.

Though I admit the posters of Bushisms were very funny.

Ironically, though Afghanistan was a more justified intervention, the Taliban are now back in control there, whereas the government put in place in Iraq has continued, maintaining at least a level of democracy and Western alignment, albeit in a highly fragile way, plagued with corruption and dysfunctionality. But given the vicissitudes along the way this is not sufficient to justify the war.

I can remember the specific article which flipped me on this one - it was, I believe, by David Willetts on Conservative Home, though the fact that I cannot now find it suggests I may be wrong about this. If anyone does know of it, please comment and I’ll add a link.

Of course, everyone does pay tax, such as VAT - but income tax is the most visible form of taxation.

This is for a number of reasons, including reducing the propensity of people to work or businesses to invest, creating ‘dead-weight loss’ and distorting economic incentives, as well as because the private sector is more likely to spend it on economically useful activity than the public sector (with some exceptions). I don’t want ‘no tax’, but would rather something like 30% of GDP, compared to the 33% pre-pandemic, let alone the 38% we are currently headed for.

National Insurance is a strictly worse tax than income tax as it only affects working age people, whereas income tax affects everyone.

And no doubt my opposition to Welsh independence influenced my negative view of their actions.

Just as a test of whether a place of worship/religious community is serious is whether they see the education of the next generation as a priority.

The EU invests billions into programmes designed with the explicit purpose of bolstering a sense of European identity and solidarity.

A friend once said of same-sex marriage that he only realised what it was important (as opposed to civil partnerships) when he listened to some of those who were strongly opposed. Similarly, there is nothing to make one support more initiatives for patriotism than to watch the scoffing of a certain portion of the educated elite that meets even the mildest suggestion.

To be clear, I am not suggesting that Olusoga should be banned from expressing his views, or fired from his academic post, or that a commercial company should not be allowed to make such a programme. I am saying it should not have been a priority for the national broadcaster, funded by the license payer.

Yes, correlation is not causation, but when almost our entire educational and cultural institutions embark upon a sustained campaign to inculcate shame in our nation and history, and simultaneously attitudes among young people shift in this direction, I’m going to go with this being a contributory - even if not the sole - cause.

It could replace the Public Sector Equality Duty.

Each individual university is almost solely responsible for determining the curriculum, assessment and standards for their degrees, as well as what proportion get Firsts, 2:1s and so forth.

I still do think that specific change - which changed the accrual rate for pension that had already been earned from RPI to CPI - was very shabby, due to its retroactive nature. I would generally restrict pension changes to how future pensions are built up (for existing and future public sector workers), not changing existing built up entitlements.

The Financial Crisis threw this into stark relief.

I knew people who took early retirement with it at 55 and no reduction.

However, this has now been heavily mitigated by the removal of the requirement to take out an annuity as soon as you retire.

A classic ‘can I believe it?’ case.

This last is obviously not the case for doctors, nurses and teachers.

Other peculiarities of public sector pension schemes include the fact that they vary so much between different parts of the public sector, for historical rather than economic or market conditions, or the fact that employee contribution rates can be relatively high (which is causing an increasing minority to opt-out altogether) and, in a weird ‘progressive’ way, get significantly higher as you get paid more - which can cause someone to see their take-home pay actually decrease when they get a pay-rise.

There is an issue here which we’ve not even discussed in that as most public sector pensions (except the Local Government Pension Scheme) are unfunded - i.e. the money goes into the Treasury rather than being invested to pay out future contributions - this builds up massive future liabilities for taxpayers. Shifting to a defined contribution scheme would also be an opportunity to move to a funded scheme, which would be much healthier for the UK’s long-term financial position.

Or perhaps ‘right-coded’ and ‘left-coded’ are better terms.

In an older era Welsh cultural preservation was of interest to the wider political spectrum, eg "Cymru Fydd" in 19th century which sought distinction from how Irish nationalism was developing. I think its tribal valence (preceding but intensified by latest culture war developments) have kept it out of view of c/Conservatives which is a shame. Quite striking that in my Welsh medium school in 90s/2000s you would have a huge emphasis on hymns, older poetry, culture, patriotism, ties to the chapel specifically, in a way that had gone firmly out of fashion in English schools even then.

Although somewhat transmuted in the "officialdom" version which is quite progressive-tinged, still a lot that would be appealing to small-c conservatives.

While I agree with you that the Iraq war was a new negative for western countries and a mistake to engage in (especially given how it strengthened Iran), saying ISIS and the ensuing chaos caused as many problems as Saddam did underestimates just how bad Saddam was. Between Kuwait, Iran/Iraq war, and the kurds, he killed about a million people in people in wars of choice. ISIS never got close to that.